The RBA governor’s speech to the Australian Business Economists annual dinner last week was a canny exercise in misdirection, focusing on the rising price of dental visits, haircuts, sporting and other recreational activities while omitting key facts about the sources of inflation that have resulted in a dramatic fall in Australian living standards.

It may come as no surprise by now that after 13 rate rises since May last year, using interest rates as the sole tool for controlling inflation isn’t going to cut it.

Contrary to what Michele Bullock would have us believe, this inflation is not “homegrown”. It is global and largely the result of supply-side shocks and additional post-pandemic disruptions, exacerbated by the ability of companies to leverage their market dominance, increasing prices beyond what is strictly necessary. The RBA’s own research has acknowledged this.

As far back as February, the RBA was acknowledging that supply shocks, not demand, accounted for at least 50% of inflation increases, including the war in Ukraine and pandemic- and climate change-related supply-chain disruptions. Its more complex in-house structural model of the economy found that supply shocks actually accounted for three-quarters of the recent inflation.

And in the minutes of its November meeting, the RBA all but admitted that — to quote Glenn Dyer and Bernard Keane — “business arrogance and greed was behind inflation”.

“Members also observed that, while longer-term inflation expectations remained broadly anchored, there had been signs of a slight upward drift in some financial market measures of inflation expectations,” the RBA’s statement reads. “If sustained, this would contribute to higher inflation. Furthermore, members noted growing signs of a mindset among businesses that any cost increases could be passed onto consumers.“

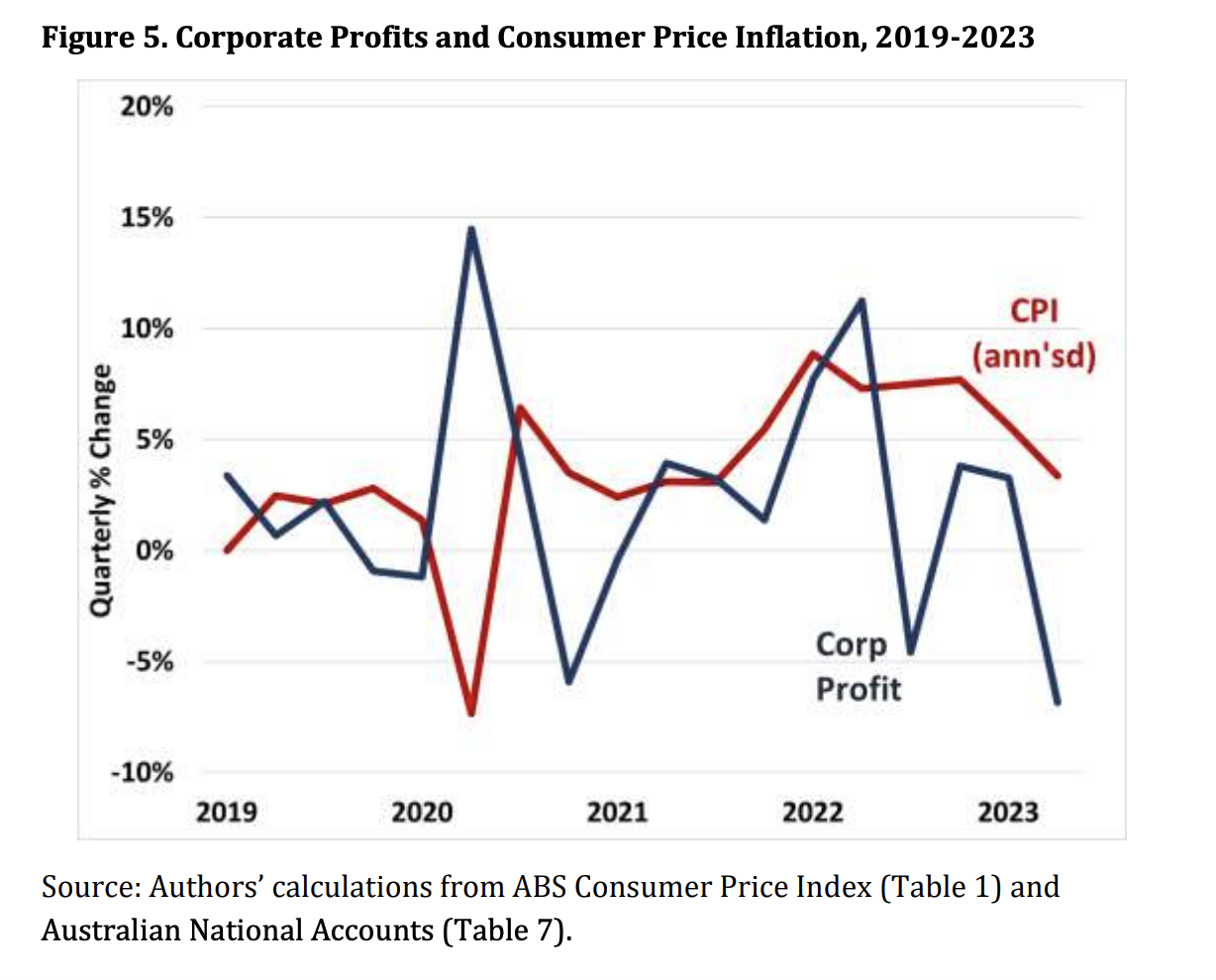

While excess profits have moderated this year along with inflation, they are still well above historical norms in both dollar terms and as a share of GDP. A graph from a report by the Australia Institute’s Centre for Future Work shows the close correlation between changes in profits and annualised consumer price index (CPI) inflation, reinforcing the view that the two are linked both on the way up, and on the way down.

And as economist Alan Kohler recently pointed out, when rates increase, “not only do we pay more to the banks for our mortgages, but the Reserve Bank, that we own, also forks out an extra billion dollars to them as well”, thanks to post-pandemic changes on overnight lending and interest earned on exchange settlement deposits (bank deposits held by the RBA), which increased from around $25 billion before the pandemic to $362.5 billion now.

Dividends surged by $75 billion between 2020 and 2023 (Centre for Future Work from ABS data) — a 65% jump — yet the RBA remains silent on its effect on spending power and inflation. It’s pretty contradictory for the RBA to wring its hands about the threat of higher wages while saying little about higher profits and dividends in the hands of investors.

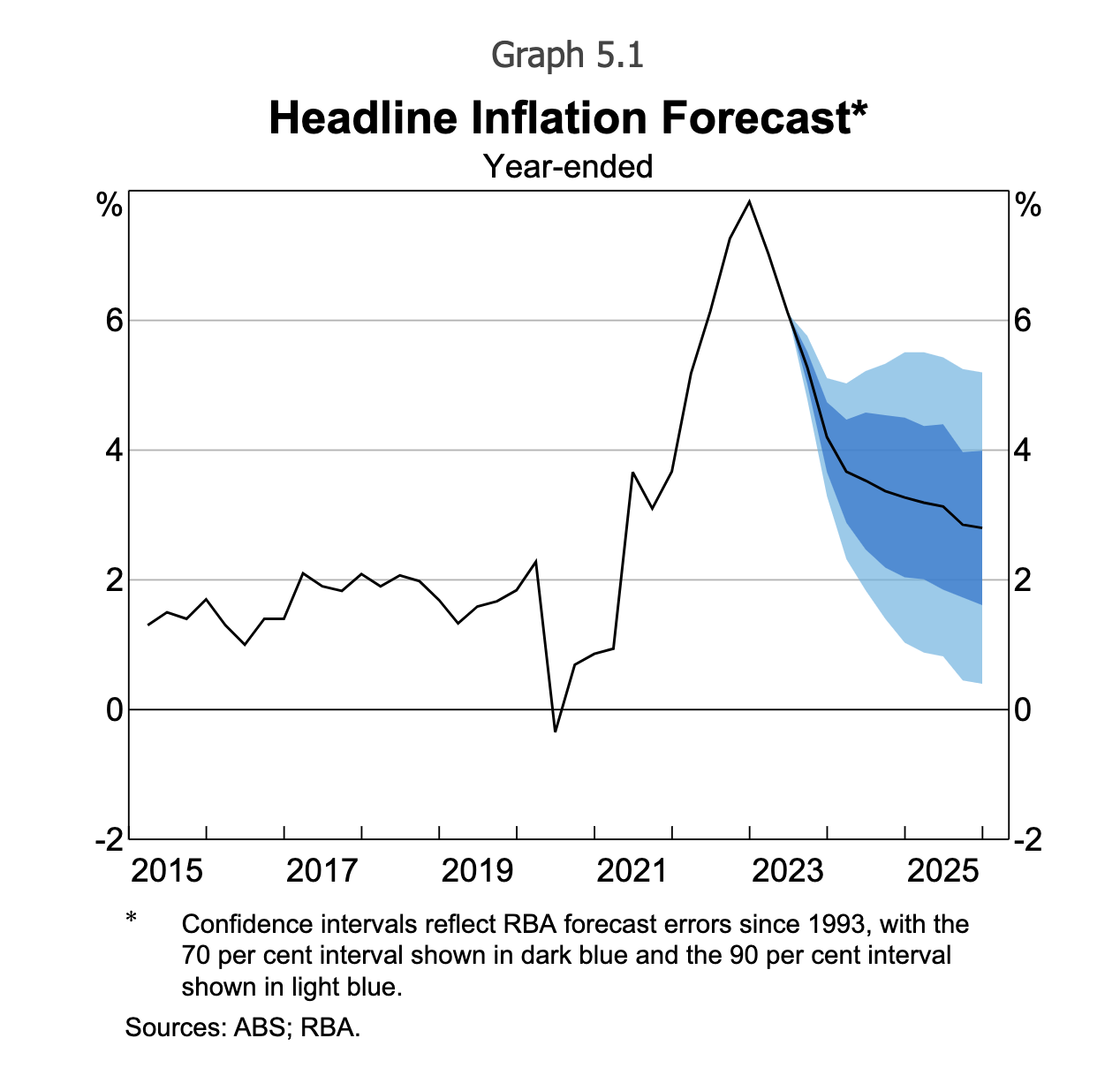

And with the $21 billion stage three tax cuts in the pipeline (unless Treasurer Jim Chalmers comes to his senses), inflation is likely to worsen. A graph in the RBA’s August CPI forecast shows a predicted jump in inflation in the second half of next year, which just so happens to coincide with when the tax cuts are due to kick in.

It seems curious that this also wasn’t worthy of mention in either the minutes of this month’s board meeting, the economic outlook section of the statement on monetary policy, nor Bullock’s speech. (Though it did come up in the Q&A where she acknowledged that though it was not her place to “comment on the government’s stage three tax cuts, they are already factored into our thinking about monetary policy”.)

No, better to blame it on the rising price of dentist visits and haircuts. Never mind that regular dental appointments help prevent and reduce instances of heart disease and thus the strain on the already overburdened health system. To imply that regular check-ups and haircuts might help increase rates is just irresponsible. (Though if Bullock is so concerned about rising prices, she might want to consider a word with Chalmers about competition policy before its ability to control private bank lending is revoked, and its relationship with Treasury formally severed.)

It’s also pretty hard to explain how this inflation is homegrown when real household disposable income per capita decreased by 5.1% over the past financial year, resulting in massive falls in people’s living standards, according to the Australia Institute’s Greg Jericho.

But weirdly, the economy still grew by 3% in 2023, and by 4.3% in 2021-22. Clearly somebody is enjoying the spoils. (Hint: it’s not households.) For that you’d need to look at some of Australia’s major profit centres: mining (which accounts for about half of all corporate profits in the economy), banking and finance, manufacturing, supermarkets, utilities, telcos, Qantas, etc.

Australian fossil-fuel exports increased 9% this year to a record $460 billion. The finance sector reported a gross operating surplus of $110.5 billion in the 2022-23 financial year, making it the second largest source of profits in the Australian economy after mining. Coles and Woolworths recorded a $1.6 billion profit in August, a nearly 5% increase on 2022 and a nearly 20% rise in earnings. Qantas posted a record $2.47 billion full-year underlying profit, an 18.2% increase in domestic earnings before interest (an indication of profit margins), and an 11.7% increase in international margins, including freight, backed by strong travel demand, high ticket prices, the sacking of 1,700 workers, cancelled flights and unredeemed travel credits.

If anyone needs a haircut, it’s the companies running monopolies on goods and services — companies that can jack up prices with no pushback from government, regulators or the Reserve Bank, knowing full well it’s their customers that will end up paying for it.

You feeling the pain, reader? If so, we want to hear from you — especially while our comments are closed due to our website upgrade. Send us your thoughts on this article to letters@crikey.com.au. Please include your full name to be considered for publication. We reserve the right to edit for length and clarity.

Crikey encourages robust conversations on our website. However, we’re a small team, so sometimes we have to reluctantly turn comments off due to legal risk. Thanks for your understanding and in the meantime, have a read of our moderation guidelines.